From 1 March 2026, the gender-based undervaluation (GBU) award increases changed how wages funded under the Worker Retention Payment (WRP) may appear in payroll systems.

While the overall hourly rate for employees may remain the same, the structure of that rate may change depending on how your payroll system is structured. As a result, part of the WRP funding may now be absorbed into the base award rate rather than appearing as a separate allowance (click here if you are uncertain about your payroll position).

For approved providers, this creates an important reconciliation consideration. Once part of the WRP moves into the base rate, it may no longer be clearly identifiable within payroll reports, even though the funding is still being applied to employee wages. Services should therefore ensure they have a clear method of tracking WRP expenditure, particularly where part of the WRP has been absorbed into the base rate following the award increase.

→ IMPORTANT: Providers should also ensure that employee wage rates implemented in payroll systems are consistent with the minimum rates published by the Department of Education for the Worker Retention Payment program. These rates can be accessed here.

→ Advice on your WRP Annual Declaration in light of gender-based undervaluation:

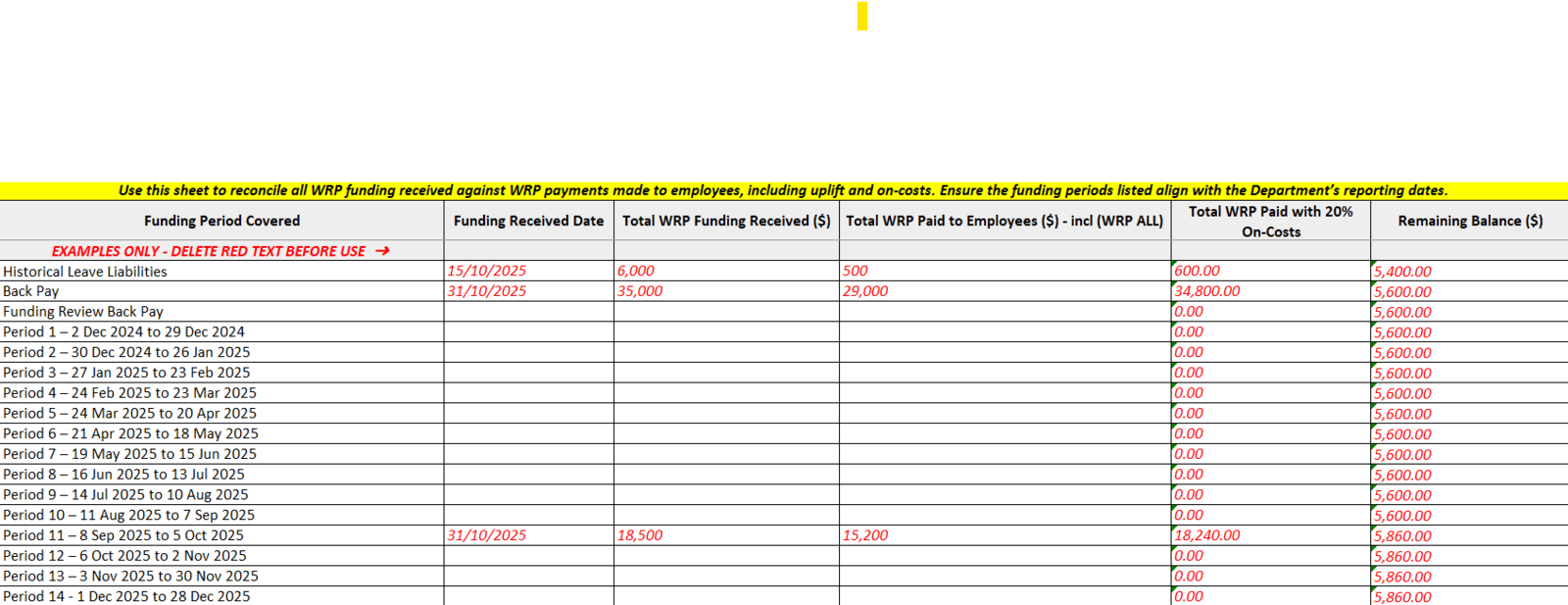

To support services in managing these changes, we recommend that providers begin reconciling their WRP expenditure against WRP funds received for the period 1 July 2025 to 28 February 2026, in preparation for the annual declaration.

As discussed, from 1 March 2026, reconciliation is likely to require a different approach due to the implementation of the gender-based undervaluation changes.

However, by organising and reconciling the earlier period now — where WRP was more clearly distinguishable — you can establish a structured baseline. This will help reduce complexity and make the reconciliation process from 1 March onward more manageable.

Following the GBU changes, services generally fall into one of two payroll approaches.

The first is where an employee’s hourly rate is presented as a single combined rate that already incorporates the WRP component. In this structure, the payslip may simply show the employee’s hourly rate with no separate WRP allowance line. Internally, however, part of that hourly rate still represents WRP funding.

The second approach is where services continue to present a base award rate and a separate WRP allowance. Under this structure, the award base rate increases following the GBU decision, while the WRP allowance decreases. The employee’s overall hourly rate remains unchanged, but part of the WRP funding is now absorbed into the higher base rate.

In both approaches, the key principle remains the same. The location of the WRP funding may change, but the funding itself must still be accounted for.

A practical way for providers to track WRP expenditure is through a simple reconciliation process outside the payroll system.

Under this approach, services track the hours worked by eligible employees and multiply those hours by the employee’s original, pre- 1 March 2026 WRP hourly amount.

This works because the original WRP hourly amount remains the same, even if part of the funding has moved into the base rate following the award increase.

For example, if an employee previously received $3.74 per hour in WRP funding, the total WRP applied to their wages can be calculated by multiplying the hours they worked by $3.74.

If that employee worked 60 hours during a pay period, the total WRP applied to their wages for that period would be:

60 hours × $3.74 = $224.40

This methodology captures the full WRP component, regardless of whether part of that funding is now appearing within the base rate or as a reduced WRP allowance.

Services should maintain a clear reconciliation record that demonstrates the relationship between WRP funding received, WRP funding applied to employee wages and how the gender-based undervaluation changes have impacted funding allocation.

A simple reconciliation worksheet can include:

employee name

hours worked in each pay period

the employee’s pre-1 March WRP hourly amount

total WRP applied to wages for the period

Your reconciliation records: Option 2

Some providers may prefer to reconcile WRP expenditure by separately tracking:

the WRP allowance recorded in payroll, and

the portion of WRP that has been absorbed into the base rate.

Under this approach, services create a simple register or spreadsheet listing each employee and the amount of WRP per hour that has been absorbed into their base rate following the GBU award increase.

For example, if an employee previously received $3.74 per hour in WRP funding and their current WRP allowance recorded in payroll is $2.50 per hour, the remaining $1.24 per hour represents WRP funding absorbed into the base rate.

A reconciliation worksheet may therefore track:

employee name

hours worked in each pay period

WRP allowance recorded in payroll

absorbed WRP amount per hour

total WRP applied to wages

In this example, WRP expenditure could be calculated by multiplying the employee’s hours worked by both the WRP allowance and the absorbed WRP amount and combining those figures.

Maintaining correct payslips for staff

Where providers use this manual reconciliation approach, it is important that payroll systems continue to correctly present the new wage components on employee payslips.

This includes displaying the base hourly rate and any remaining WRP allowance where applicable. The reconciliation process should operate alongside payroll reporting rather than replacing the correct recording of wage composition within payroll.

In other words, the reconciliation worksheet is used to track WRP funding for internal reconciliation while the payroll system continues to record wages in accordance with the Department’s outlined base wages and new WRP allowance amounts.

The information provided in this article is intended as general guidance only. It does not constitute financial, accounting or legal advice.

Approved providers should consider discussing the implications of any payroll configuration or reconciliation approach with their accountant, bookkeeper or payroll professional before implementing changes. Professional advice can help ensure that payroll systems, financial records and reconciliation processes are appropriate for the circumstances of the service and compliant with relevant program requirements.

Should you require further assistance, access our below resources:

→ Gender-based undervaluation reclassification matrix

→ Gender-based undervaluation factsheet for employees

→ Gender-based undervaluation webinar replay